Higher prices and a deteriorating economic environment have started to take their toll on oil demand, but strong power generation use and a recovery in China are providing a partial offset. Global oil demand growth has been marginally reduced to 1.7 mb/d in 2022, reaching 99.2 mb/d. A further 2.1 mb/d gain is expected in 2023, led by a strong growth trajectory in non-OECD countries.

Rarely has the outlook for oil markets been more uncertain. A worsening macroeconomic outlook and fears of recession are weighing on market sentiment, while there are ongoing risks on the supply side. For now, weaker-than-expected oil demand growth in advanced economies and resilient Russian supply has loosened headline balances. Benchmark crude futures have tumbled by more than $20/bbl since early June, trading below $100/bbl at the time of writing. Yet, persistent physical crude price tensions and extreme refinery margins highlight underlying imbalances for crude and products supply.

In its latest update the World Bank warned that Russia’s invasion of Ukraine and its effects on commodity markets, supply chains, inflation and financial conditions have accentuated the slowdown in global economic activity. The bank now expects world GDP growth to ease to 2.9% in 2022 from 5.7% in 2021. The IMF has cautioned that a recession next year cannot be ruled out, given the elevated risks.

The deceleration of economic activity is adding further uncertainties to our oil demand forecast but, for now, we have only modestly trimmed our outlook for 2022 and 2023. High fuel prices have started to dent oil consumption in the OECD, but this was largely countered by a stronger-than-expected demand rebound in emerging and developing economies led by China as it starts to emerge from Covid lockdowns. Oil demand is now expected to expand by 1.7 mb/d in 2022 and 2.1 mb/d next year, when it reaches 101.3 mb/d.

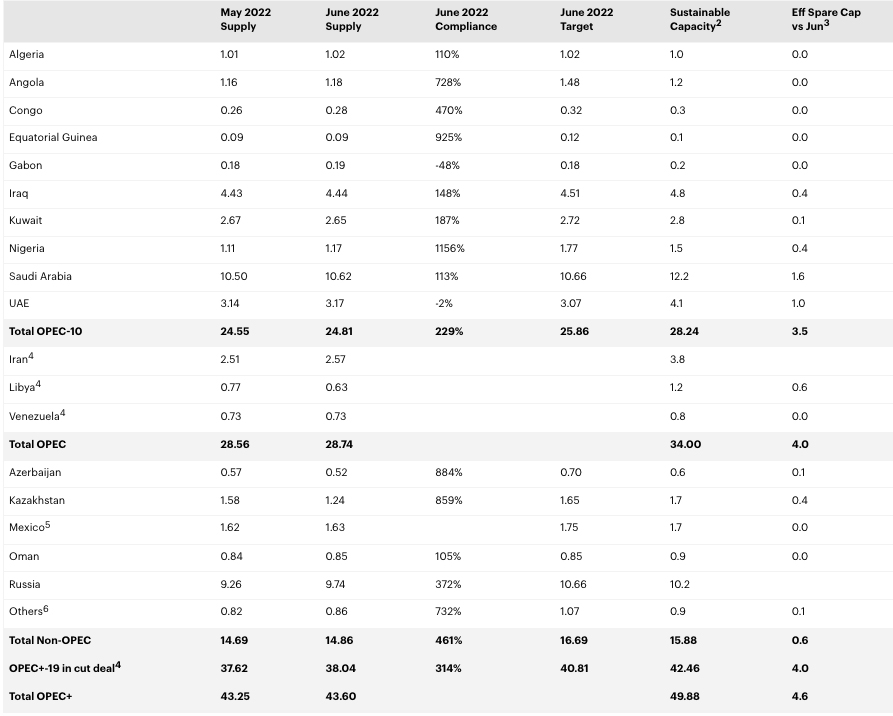

Our forecast was revised slightly higher for oil supply for the remainder of the year due to Russia’s surprisingly strong performance. In June, global output rose by 690 kb/d to 99.5 mb/d, as Russia defied sanctions and the US and Canada pumped more. While world oil supply is expected to grow by roughly 1.8 mb/d through December, rising short-term risks to oil supply in Kazakhstan, Libya and elsewhere have put the spotlight on spare capacity, which now is held primarily by Saudi Arabia and the UAE. Their combined buffer could fall to just 2.2 mb/d in August with the full phase out of record OPEC+ cuts.

The OPEC+ group is due to meet on 3 August to chart strategy for September and possibly longer. Global oil inventories remain critically low, with recent builds concentrated in China, where refiners reduced runs due to weaker demand amid Covid lockdowns. OECD industry stocks have recovered somewhat thanks to sizeable government stock releases, but remain nearly 300 mb below their five-year average. As an EU embargo on Russian oil is set to come into full force at the end of the year, the oil market may tighten once again. With readily available spare capacity running low in both the upstream and downstream, it may be up to demand side measures to bring down consumption and fuel costs that pose a threat to stability, most notably in emerging markets. Without strong policy intervention on energy use, risks remain high that the world economy falls off-track for recovery.

Source: IEA